2026 mortgage lead gen reality check: What’s working, what’s risky, and what to fix now

The mortgage market doesn’t need another “trend report.” What it needs is a reality check—one that connects what’s happening in the economy to what’s happening inside your lead pipeline, your dialer, and your compliance workflows.

That’s exactly what we set out to do in ActiveProspect’s Financial Services webinar, “The 2026 Mortgage Lead Gen Reality Check.” Moderated by Andrew Bailey (Content Strategist at ActiveProspect), the session featured two familiar voices for mortgage marketers:

- Emma Bernstein, who leads ActiveProspect’s Financial Services vertical.

- John Henson, a longtime mortgage attorney and lead gen specialist at Henson Legal with nearly two decades of perspective on what’s changing—and what never does.

From rates and market uncertainty to consent language, AI voice, and list hygiene, the conversation circled one core truth: In 2026, lead generation isn’t just a marketing channel—it’s a risk and performance system. And the teams who win will be the ones who treat it that way.

Below is a recap of the biggest takeaways and the practical steps you can apply immediately.

Key takeaways

- Mortgage market uncertainty is the norm in 2026 (rates, Fed/politics, low home sales, increased scrutiny/litigation).

- All real estate is local: Don’t over-index on national headlines—optimize to your ZIP/county and local data.

- Smaller shops can’t copy the Rocket playbook—win with a local strategy and processes you can actually run well.

- “Cheap leads” can get expensive fast: Low CPL often means higher downstream costs (time, compliance risk, low funded-loan yield).

- Trust but verify your lead sellers: If they can’t explain traffic sources, show the form, and walk through consent language, it’s a red flag.

- When you buy leads, you’re buying the seller’s compliance program—know exactly what the consumer saw and agreed to.

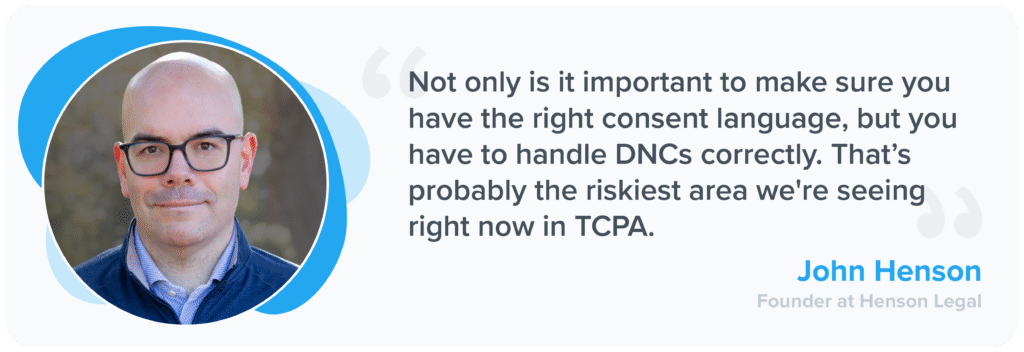

- TCPA risk often comes from process gaps: One-off texting/dialing outside systems, not reviewing disclosures, and no proof-of-consent “system of record.”

- DNC/list hygiene is a major risk area: Failure to disposition opt-outs correctly (especially in pooled lead models) leads to repeat calls and exposure.

- Audit during onboarding: Map ad → form → submit, confirm when the lead is sold, and validate consent language at that moment.

- AI can amplify bad practices: Don’t “throw AI at questionable leads”—it scales problems (consumer frustration, complaints, spam reputation).

- Outbound AI voice needs extra care: Ensure consent language covers AI voice and that providers can articulate their compliance approach.

- Protect phone reputation (“Spam Likely”): Avoid high-volume, short-duration, repetitive calling patterns—especially with AI.

- Use tech to add guardrails: Document and verify consent with TrustedForm and apply real-time filtering and routing with LeadConduit so only qualified leads reach reps.

Let’s dive deeper into the topics presented above.

The 2026 mortgage market: Uncertainty is the baseline

John kicked off with the macro view: Mortgage marketers are operating inside a triangle of uncertainty—rates, politics/Fed leadership, and industry pressure from both regulation and litigation.

He pointed to a sobering stat: 2025 was the lowest year for home sales in nearly 30 years, a reality that naturally constrains volume for lenders and stresses partner ecosystems like realtors. That uncertainty isn’t just economic—it changes behavior. Consumers hesitate. Realtor relationships tighten. And lenders compete harder for a shrinking pool of mortgage leads.

At the same time, John noted growing scrutiny in the real estate ecosystem—referencing high-profile pressures like steering and RESPA-related lawsuits that influence how adjacent platforms operate and how cautious participants become. The result is a market where everyone is trying to re-evaluate: Who are my buyers? How do I expand the buyer pool? Who will still be buying in 2026 and beyond?

“All real estate is local,” and that’s reshaping lead gen

One of the most resonant themes of the webinar was John’s comment that “there are two mortgage markets now.” National trends matter, but they don’t always reflect what’s happening in your ZIP code.

He shared an example: National stats might show a downturn, but a local operator could be up year-over-year. Some regions lag national averages by months. Others lead them. That gap creates a dangerous trap: Mortgage teams that overreact to headlines rather than adapting to local realities.

So what should mortgage marketers do?

Lean into local advantage, especially if you’re not Rocket

John highlighted a real shift he’s seeing: Smaller shops are leaning harder into local marketing, both digital and analog. Yes, analog marketing.

Think:

- Showing up at community events

- Strengthening realtor relationships

- Being visible where local buyers actually live (online and offline)

- Combining targeted digital with human presence

It’s not nostalgia. It’s strategy. When national lenders have systems optimized to the millisecond, smaller teams win by being present, relevant, and operationally consistent in the markets they can actually dominate.

The Homebuyer Privacy Protection Act: Trigger leads shift, not disappear

A major regulatory note was the Homebuyer Privacy Protection Act, which John said is now in place and generally viewed positively because it aims to minimize trigger leads—the flood of calls, texts, and emails consumers receive after a credit pull.

But he cautioned against assuming it eliminates all “lead-like” outreach:

- There are exceptions, particularly for the originating lender or current servicer.

- It doesn’t stop other common consumer confusion, like mail solicitations after signing.

- And it doesn’t affect situations where the consumer opts in directly online—because consent changes the equation.

The key message: Consumer expectations are shifting, and marketers need to align both compliance and customer experience accordingly.

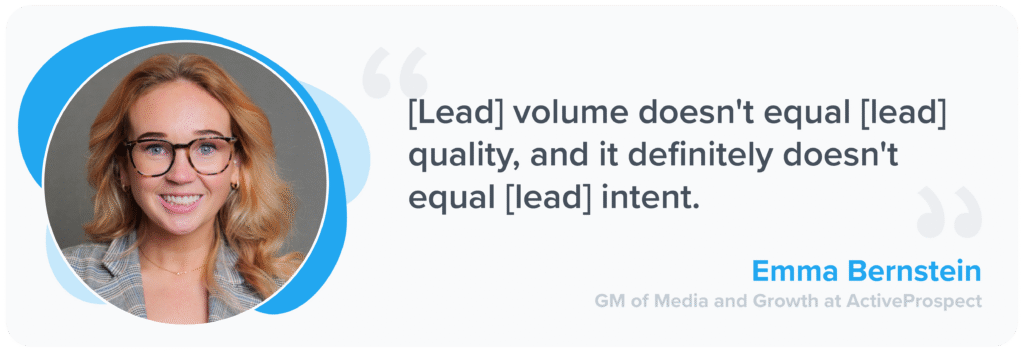

Why “cheap leads” often cost more than premium leads

When the conversation shifted to lead buying strategy, Emma emphasized something many new buyers learn the hard way:

Smaller mortgage companies and individual loan officers often start with lists because they feel tangible. But if you optimize for lowest cost per lead, you may be ignoring the costs that actually determine ROI:

- Sales time wasted on low-intent contacts

- Downstream conversion issues

- Compliance and reputational exposure

- Low funded-loan yield (the metric that truly matters)

John reinforced this with a pattern he’s seen repeatedly: Local retail loan officers are used to closing at extremely high rates once they’re face-to-face. Then they buy low-cost leads, don’t reach half the list, don’t convert at anything close to prior rates, and conclude “lead gen doesn’t work.”

The truth is more nuanced: Lead gen can work, but it requires a different playbook, and the right expectations.

“Trust, but verify”: The lead vendor transparency test

If there was one phrase that anchored the webinar, it was Emma’s: Trust but verify.

Her advice was blunt: If your lead seller cannot explain where their traffic comes from—even in general terms—or show what the consumer journey looks like (the form, disclosures, and consent language), that’s a red flag.

John took it a step further with a line every mortgage buyer should remember: “When you’re buying leads, you’re buying their compliance program.”

That framing changes everything. You’re not just purchasing a contact record—you’re purchasing:

- How consent was captured

- What was disclosed

- What the consumer reasonably expected

- And what you can legally do next

Where TCPA risk creeps in (even when no one is trying to break the rules)

Emma outlined four of the most common ways mortgage teams unintentionally open themselves up to TCPA risk:

- Assuming the seller handled compliance

- Not reviewing the consent language connected to the lead

- One-off texting and dialing outside systems of record

- No system of record for proving consent later

That last point is critical. In the world of TCPA claims, if you can’t prove consent, it’s almost like it never existed.

John added another high-risk scenario that shows up in distributed sales models: The “mothership” buys leads into a pool, a loan officer calls, the consumer says “don’t call me,” but the rep doesn’t disposition correctly—so the lead goes back into the pool and gets called again.

That’s how companies rack up DNC violations without realizing it. And the fix to that isn’t just consent—it’s list hygiene and workflow discipline.

Auditing consent without slowing down sales

The audience asked a smart question: How do you audit consent without slowing sales? John framed it in two layers:

1. Vendor onboarding audits

If you’re onboarding a new lead source, you need to understand the flow end-to-end:

- What does the consumer see from ad to submit?

- At what point is the lead sold?

- What does the consent language say at that moment?

He even shared a real example of audits where leads were sold before the final submit—meaning the buyer thought they were purchasing a fully consented lead when the consumer hadn’t completed the process.

2. Operational audits in-market

Once leads are flowing, you need a reliable way to tie:

- lead → site → session → disclosure → consent

so you can be confident that when you put that lead back into a dialer cadence, the consent still matches what you’re doing.

AI voice in mortgage: Powerful, yes—but consent must catch up

AI was (predictably) one of the biggest topics of the session—and one of the most nuanced.

John separated AI voice into two categories:

- Inbound AI voice (think smarter IVR): Typically lower risk

- Outbound AI voice: Doable, but requires more careful compliance

The big point: Traditional marketing consent may not be enough for outbound AI voice. If your consent language only says, “I agree to receive marketing calls about mortgage,” that might not adequately cover AI voice outreach. John’s guidance: Your consent language should explicitly reference AI voice if that’s part of your strategy.

He also highlighted an operational risk many teams underestimate: Phone number reputation. AI systems are extremely good at what carriers interpret as spam behavior:

- Short call duration

- High volume

- Repeated attempts from the same number

- Low pickup rates

That’s how you end up labeled “Spam Likely”—which kills contact rates, wastes spend, and creates consumer frustration that can escalate into complaints.

Emma added the strategic warning: AI doesn’t fix broken lead programs. It amplifies them.

If you’re buying questionable leads with unclear consent and unknown sources, AI will only help you:

- Contact more people who didn’t expect to hear from you

- Faster

- More aggressively

Which is a straight line to brand and compliance risk.

How ActiveProspect fits: Structure for growth, not just lead flow

When asked how technology can help teams move fast without creating risk, Emma laid out the “structure for growth” model:

- Use TrustedForm to document and retain proof of consent

- Use TrustedForm Verify to ensure the consent language is what you expect on every lead

- Pair with LeadConduit for real-time decisioning:

- duplicate filtering

- scrubbing against known litigator lists

- routing only leads you’re confident in

- keeping questionable leads out of the hands of reps

The message: Real-time control beats after-the-fact cleanup, especially when your sales team is under pressure to hit volume targets.

Final advice for mortgage marketers in 2026

As the session wrapped, both panelists delivered practical guidance you can summarize in one sentence: Know your sources, know your consent, don’t rush shiny tools onto shaky foundations.

John’s parting advice:

- If a lead vendor says their traffic sources are “secret sauce,” that’s not a strategy—that’s a risk.

- You must understand where leads come from and what the consumer agreed to.

Emma’s closing reminder:

- Don’t chase quick wins (cheap lists, massive imports, AI blasts) at the expense of brand trust and compliance discipline.

- The consumer experience still matters—and confusion creates risk.

The bottom line

Mortgage lead gen in 2026 is about more than buying leads. It’s about building a system that can:

- Verify consent

- Protect your brand

- Move fast without breaking trust

- And consistently turn lead spend into funded loans

The teams that succeed won’t be the ones with the biggest budgets. They’ll be the ones who treat lead gen as a connected workflow—performance + compliance + customer experience, all working together.

If you want to revisit the conversation or explore how to strengthen your lead quality and consent workflows, book a free demo now—and keep an eye out for the next webinar.

DISCLAIMER: This page and all related links are provided for general informational and educational purposes only and are not legal advice. ActiveProspect does not warrant or guarantee this information will provide you with legal protection or compliance. Please consult with your legal counsel for legal and compliance advice. You are responsible for using any ActiveProspect Services in a legally compliant manner pursuant to ActiveProspect’s Terms of Service. Any quotes contained herein belong to the person(s) quoted and do not necessarily represent the views and/or opinions of ActiveProspect.